Funding Strategies to Protect Yourself Against Interest Rate Risk

last updated on Wednesday, February 18, 2026 in Advances

When evaluating the addition of longer-term assets to your balance sheet, equal consideration should be given to funding and interest rate risk management. Federal Home Loan Bank of Des Moines Advances offer a streamlined approach to both funding and hedging these assets simultaneously. By utilizing long-term, fixed-rate bullet or amortizing advances, institutions can align funding with the specific cash flow characteristics of the assets they originate.

Outlined below are three illustrative funding scenarios demonstrating how this approach may be applied across different asset types.

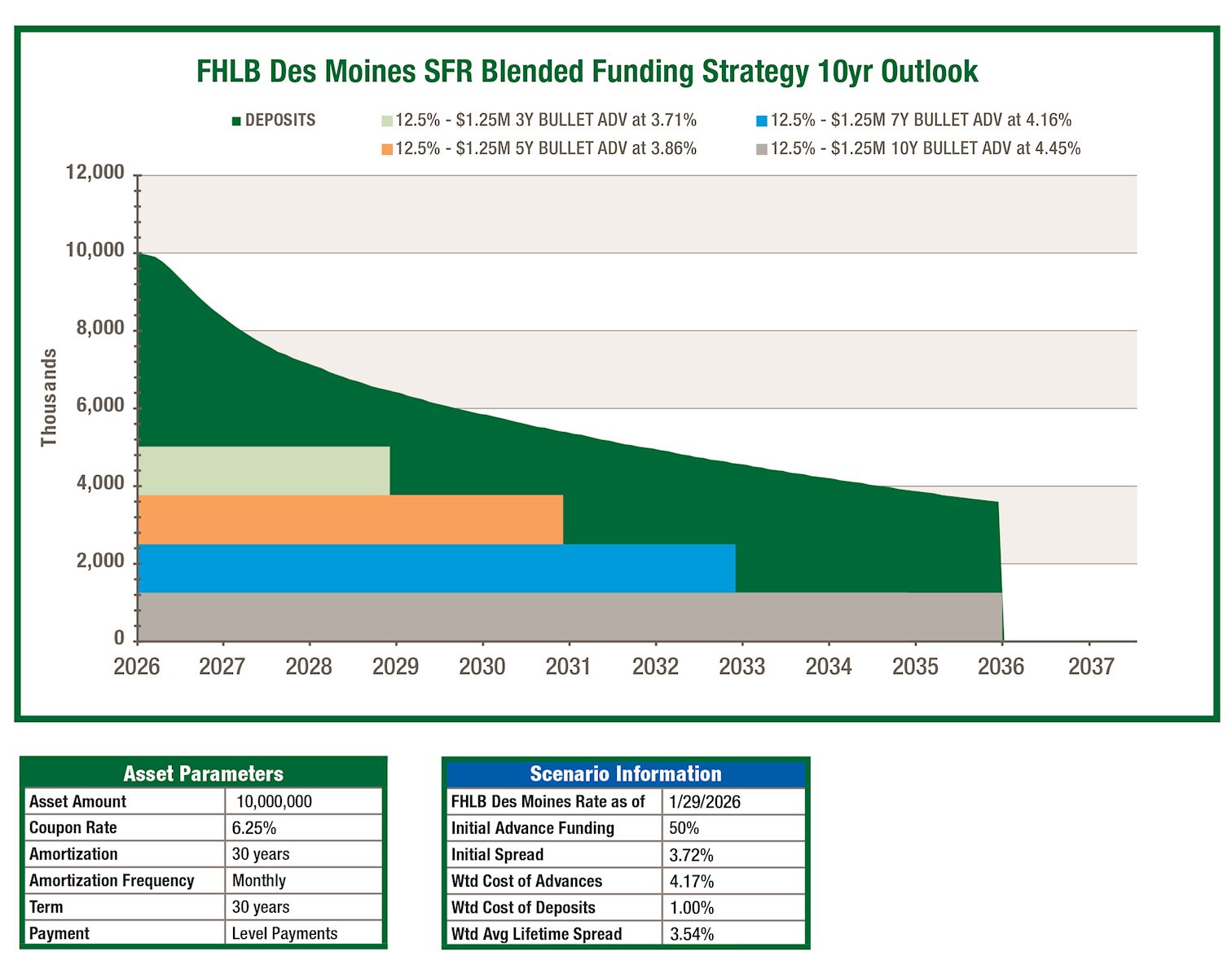

Single-Family Residential

For institutions seeking to retain residential mortgages on balance sheet while enhancing net interest income, a combination of long-term, fixed-rate FHLB Des Moines bullet advances and core deposits can be an effective funding structure.

The use of long-term advances allows institutions to lock in funding costs on a portion of the portfolio, reducing exposure to future rate volatility. Blending FHLB Des Moines advances with internal deposit funding can produce a weighted funding cost that supports spreads in excess of 200 basis points under current market conditions.

Additional considerations may include incorporating a symmetrical prepayment feature to allow for potential value realization if interest rates rise, or utilizing a Forward Starting Advance to lock in funding rates today for anticipated future portfolio growth.

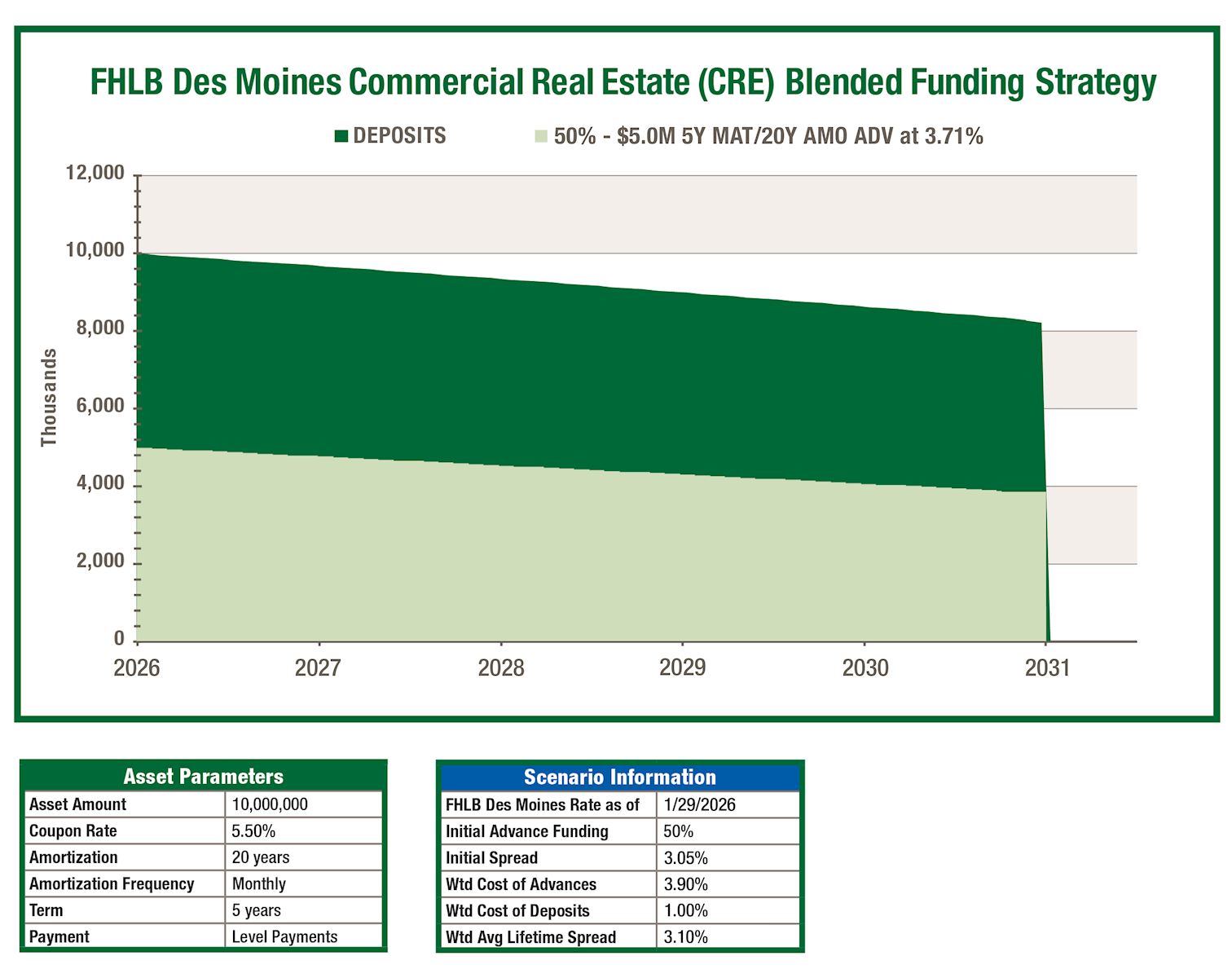

Commercial Real Estate

FHLB Des Moines amortizing advances can serve as an effective hedge for commercial real estate lending across a range of product structures. These advances allow institutions to closely align advance amortization schedules with those of the underlying loans, helping to reduce repricing and cash flow risk.

Institutions may select maturities and amortization schedules up to 30 years, as well as payment frequencies that range from monthly to annual. This flexibility enables precise alignment between asset cash flows and funding obligations.

Additional considerations include the optional inclusion of a prepayment feature for a modest premium. If the underlying loan structure allows for penalty free prepayment after a defined period, such as three years, an opt out feature on the amortizing advance can mirror that structure and eliminate prepayment costs after the same period.

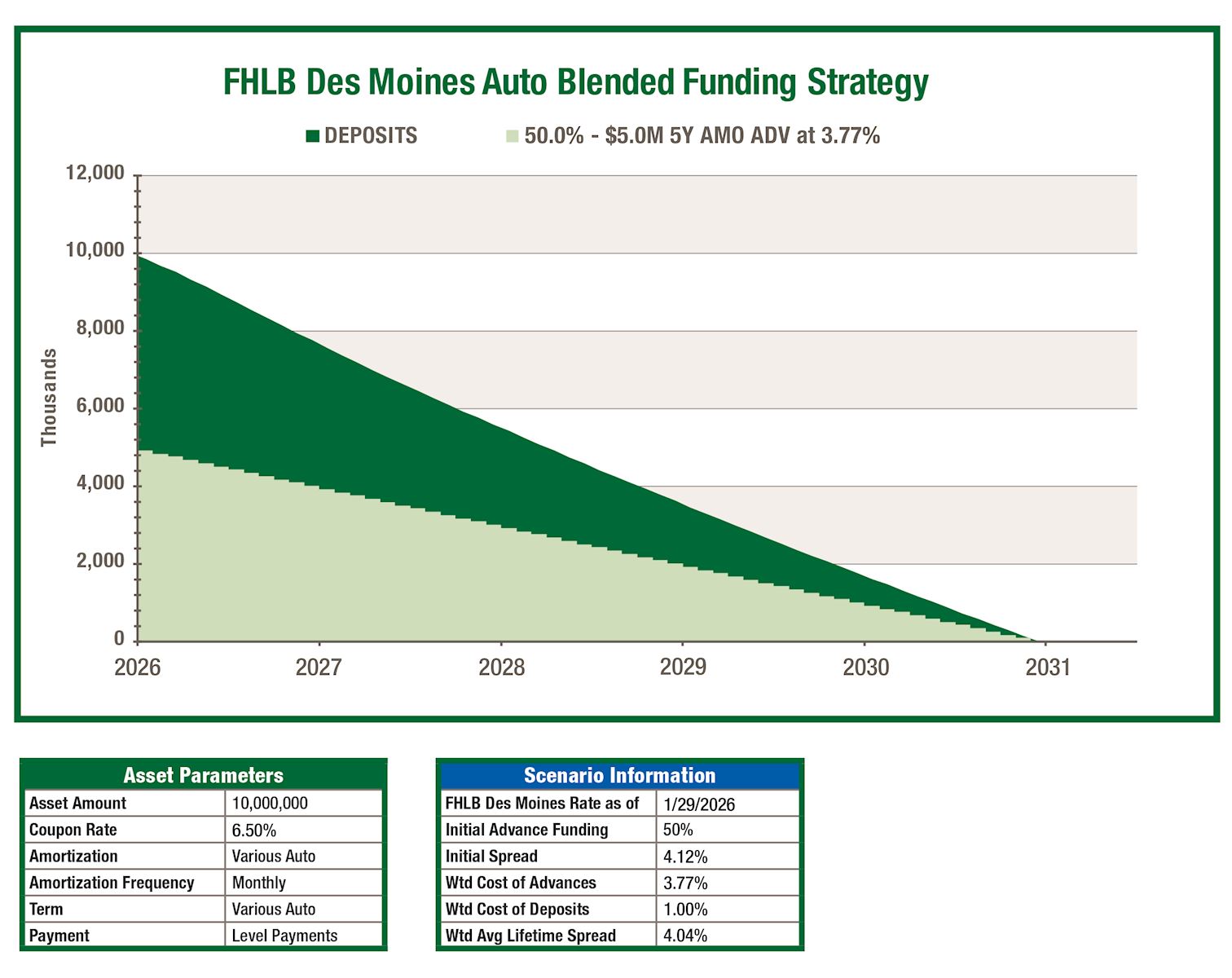

Automobile

Amortizing advances may also be used to hedge and fund a portion of an institution’s automobile loan portfolio. In the current rate environment, FHLB Des Moines advance rates in the intermediate portion of the yield curve offer competitive funding opportunities.

Matching amortizing advance structures to auto loan cash flows can help stabilize funding costs while supporting attractive spreads, given prevailing auto loan pricing.

Get Started

If your institution is planning balance sheet growth, reconsidering asset mix, or seeking to reduce rate sensitivity, this analysis provides actionable scenarios to evaluate. Your relationship manger or the Member Strategies team can provide assistance in running custom scenarios to explore how these structures may work for your institution.